It’s a late summer Saturday in central Beijing, and the sound of short, sharp beeping is quiet but relentless. In the office and shopping mall-stuffed Sanlitun area at midday – peak lunch-time in China – centipede-like queues move swiftly through 7-Eleven branches. Each customer presents their smartphone to be scanned for payment – “beep!” – before leaving with their tub of grub.

Under the shadow of the imposing Communist-style architecture of the Worker’s Stadium, it’s also rush hour for the lines of street-food vendors hawking cheap chicken wraps. Tatty pieces of card bearing QR codes are taped to their stalls – customers scan them with their phones, there’s another beep, then they’re off.

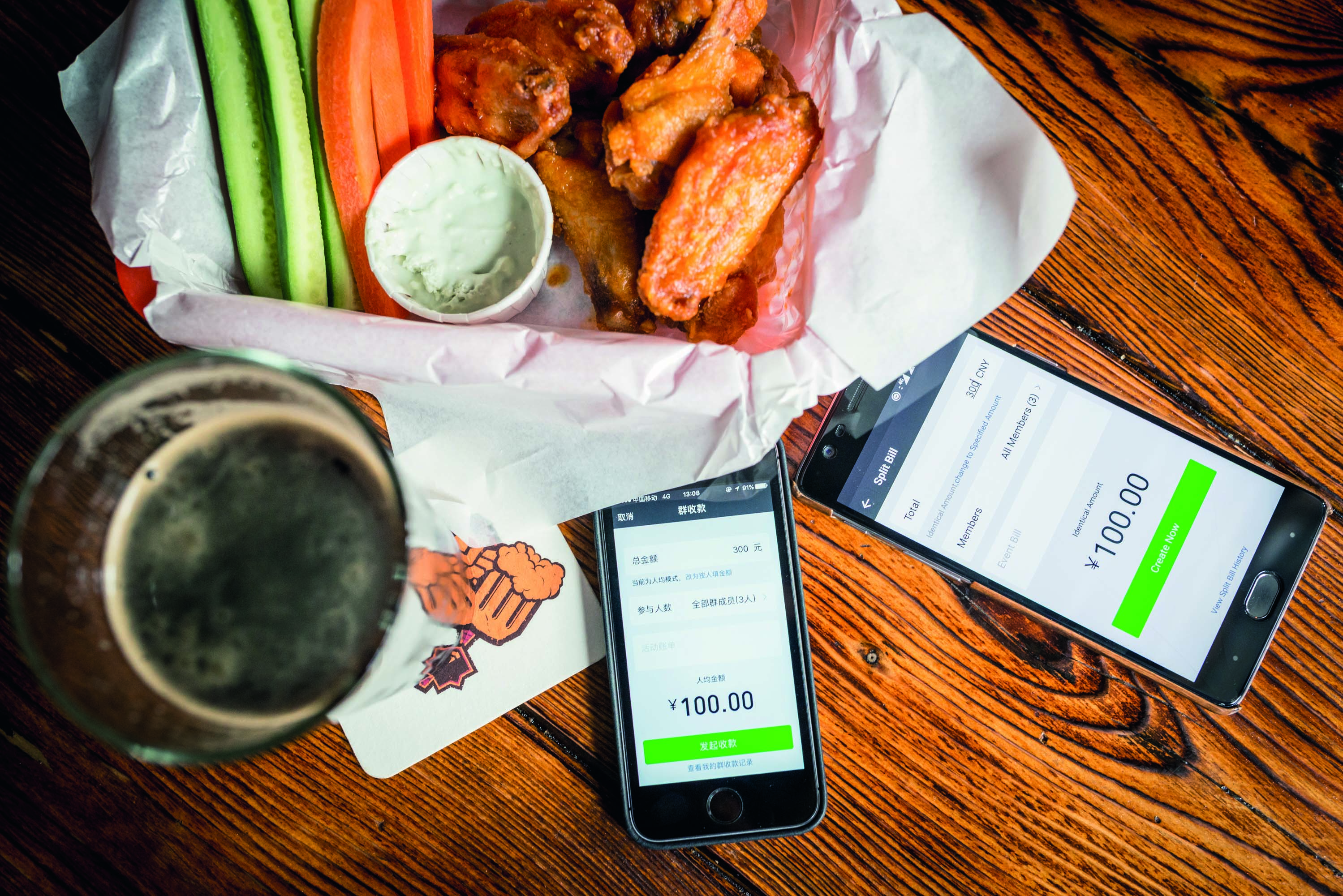

There are similar scenes in almost every restaurant in the capital – indeed, in every city across the country. Cash is out and cashless smartphone payment is in, largely via WeChat and Alipay: the two dominant cashless payment methods in the country, owned by the tech and retail giants Tencent and Alibaba respectively.

“I started paying [for most things] with my phone since early last year,” says Yuhan Xu, a 30 year-old radio researcher, as she settles a bill in a Beijing cocktail bar via WeChat. “Why? Because pretty much every shop, restaurant and bar accepts WeChat and Alipay these days – even a small pancake stall.”

This sea change in consumer behaviour was sparked in September 2014, when the store payment function on WeChat, China’s incredibly popular messaging app, was launched. Users hold money credit in their WeChat accounts and link them to their bank accounts, using it to pay retailers or other users (“I’ll WeChat you my share of the bill” is a common phrase).

“Whenever I have change in my wallet I just try to get rid of it. It’s full of germs!”

Tencent claims that over 600 million users use the firm’s payment services, including WeChat payments, with Reuters calculating that US$556bn of transactions were made using WeChat last year (Tencent takes a tiny cut of each transaction, from the receiver). Alipay works in a similar way and has about 270 million users monthly active users, with 175 million Alipay transactions made per day.

The effect of all this is summed up by Yuhan, after she stretches her arm past the drunks perched at the cocktail bar to scan the QR code sign propped up on it. “I don’t need to carry cash.”

Big data

There are ethical issues about this behaviour shift, with regard to the huge amount of personal data apps like these can store, but in China it’s pretty much accepted that companies and the government are snooping into your life. The rise of cashless payments is largely seen as a positive move that makes daily life easier. “Whenever I have change in my wallet I just try to get rid of it,” says Yuhan. “It’s full of germs!”

But what about operators? From street vendors to cafes to fast food places to high-end restaurants, for any food industry operator in China to not equip its outlets and staff to deal with cashless payments would be commercial suicide. “We found that people actually forced restaurants to have WeChat payment,” says Fan Yu, a manager at WeChat’s cashless payment department. “We’ve seen people go into a restaurant and ask if they accept WeChat payment. If they don’t, they leave.”

Today it’s unheard of to find Chinese food operators that don’t accept cashless payments, and most of them have happily embraced it. Bruno Magro, managing director of Think Food Concepts, a restaurant consultancy firm specialising in China openings, says the main benefits are obvious.

“It means that the restaurant industry is able to operate more efficiently and precisely,” he says. “Customers pay an exact amount, which decreases the margin of error upon payment. Also, cashless payment systems accelerate operation speed, compensating for time lost from queues, which benefits both the customer and service provider.”

Magro says that the initial cost of the cashless payment system – buying scanners, for example – is higher than for cash operating systems. He adds: “Another disadvantage of working with the system on a daily basis is that the contingency in loss of network and transaction failure is fairly high. Therefore staff should be trained to collect, receive and audit payments manually.”

A further disadvantage highlighted by Magro is that the nature of WeChat and Alipay means that almost no foreign tourists visiting China use them. The Chinese government’s draconian restrictions on the internet, that block many non-Chinese-owned apps, have allowed the Chinese-owned WeChat and Alipay systems to dominate their market despite being used far less in non-Chinese regions.

“Cashless payment systems accelerate operation speed, compensating for time lost from queues, which benefits both the customer and service provider”

Foreign tourists visiting China still mainly use cash over smartphone payments, so operators going too far towards cashless payments could limit income from them. “In order to promote tourism China should continue transactions through cash,” says Magro.

Faster turnover

For now at least, most food operators in China do still happily accept cash when required. Yang Ligang, manager of the Rong Ji Grandma Rabbit Head restaurant chain in the city of Chengdu in the Sichuan province, says that going fully cashless is not such a priority for mid-sized venues such as his. At his eateries, which specialise in spicy rabbit heads often eaten with a few beers, customers like to take their time eating and paying, so he’s not seen enormous benefits for his firm from the rise of cashless payments.

“It increases the turnover speed, which is the time taken from the customer sitting down to leaving – it drops from 40 minutes to 30”

But even for venues such as these, where scything through queues as quickly as possible is not so important, benefits do exist. “We don’t need much cash in store, and we don’t have to have a particular staffer to take care of the cash anymore,” says Yang. “Also, having a lot of cash in store at night was a safety concern.”

In contrast, a trip to fill up on McNuggets or chicken wings at any of Beijing’s many branches of McDonald’s or KFC really shows how operators are reaping rewards. At McDonald’s branches there are normal staffed counters but also touch screen menus. Customers order on screen, pay using their phone, then pick up the food at a special counter. It’s seamless.

Fan claims that this touch-screen cashless payment system has reduced payment time to an average of three seconds, down from 10 seconds for cash payments. “It saves a lot of work for the staff, thus reducing the cost of staffing,” he says.

He gives further examples of time saving, referring to feedback from a popular noodle restaurant chain based in the southern Guangdong province, the name of which translates to 99 Mao (with Mao being a tiny unit of Chinese currency).

“It greatly increases the turnover speed, which is the time taken from the customer sitting down to leaving – it drops from 40 minutes to 30,” he says of 99 Mao’s observations. “The system works especially well among customers familiar with the food, because they don’t need long to decide what they want. Before WeChat payments staff had to wait for the customers’ decision.”

Hitting the target

The benefits of cashless payments look set to increase for big chains. McDonald’s already runs its own app in which users can order deliveries, paid for via WeChat. Starbucks runs a popular ‘gifting’ system, which allows users to buy a coffee via WeChat payment for a friend, who claims it in-store.

Fan says that the next steps will involve WeChat introducing more targeted advertising services. “With cash payments it’s hard for restaurants to track habits. With WeChat payments, restaurants know what customers ordered according to their unique ID number and can advertise precisely. For example, if a restaurant is able to ‘remember’ what a customer ordered, the next time the customer spends money there it can recommend something similar.”

That might all sound a bit Big Brother, but this is China, where many things in business are often a bit Big Brother. But regardless of the ethical issues it throws up, cashless payment isn’t the future for the food industry here – it’s the now. The beep has been embraced.

Jamie Fullerton, with additional reporting by Paula Jin